The hydrogen fluoride (HF) gas detection market is coming into sharper focus as industrial growth, semiconductor fabrication, and stringent workplace safety standards elevate demand for reliable sensing solutions. Hydrogen fluoride, a corrosive and highly toxic gas used in petrochemicals, metal processing, and particularly in semiconductor etching processes, requires continuous monitoring and rapid alerting to protect workers, equipment, and process integrity. Market activity is being driven by technology upgrades, regulatory enforcement, and an expanding installed base of fixed and portable HF detectors across industrial, laboratory, and manufacturing environments.

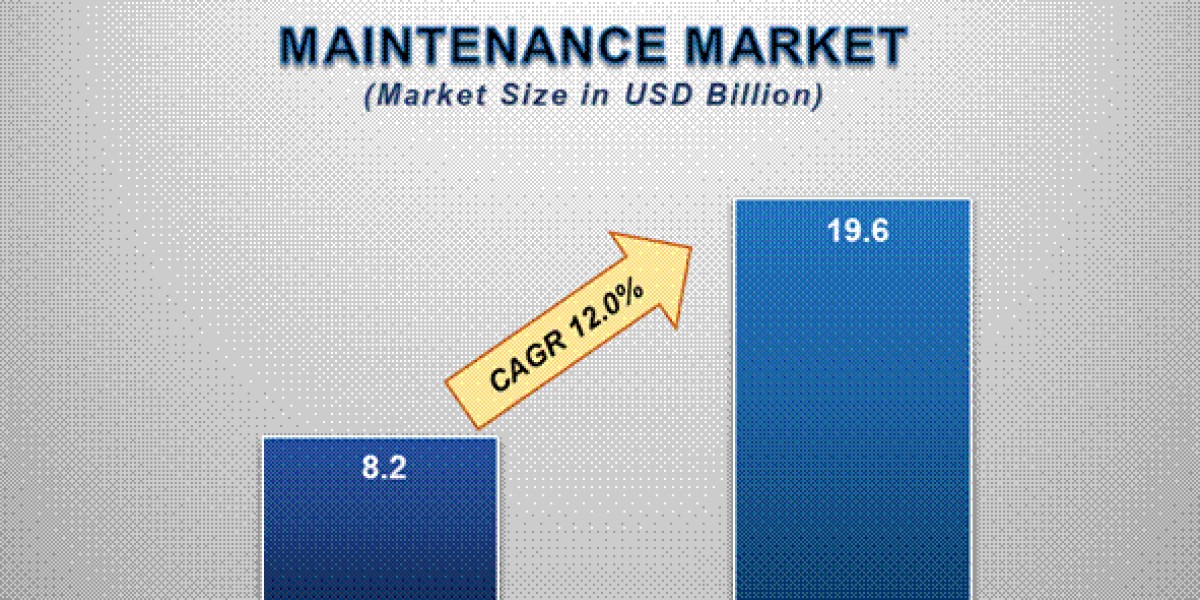

According to the research report published by Polaris Market Research, the global hydrogen fluoride gas detection market was valued at USD 546.3 million in 2021 and is expected to reach USD 880.0 million By 2030, to grow at a CAGR of 5.6% during the forecast period.

Market Summary

Hydrogen fluoride gas detection has matured from niche specialty sensors to a broader ecosystem of fixed detectors, portable monitors, sensor cartridges, and integrated networked systems. The market encompasses electrochemical and solid-state sensors, smart transmitter modules for fixed installations, personal single-gas detectors, and system-level software for alarm management and data logging. Demand is concentrated where HF is used or generated — semiconductor fabs and chemical plants, but also in research laboratories, pharmaceutical manufacture, and occasional use in oil and gas and aluminum processing. Several recent market analyses point to steady growth as end-users prioritize continuous monitoring, trace-level detection, and easier maintenance/replacement cycles for sensor modules.

Key Market Growth Drivers

Semiconductor manufacturing remains a primary growth engine for HF detection because HF and fluorinated gases are essential in wafer processing steps. As global chip fabrication scales and new facilities come online, the need to protect cleanrooms, utility corridors, and maintenance staff is accelerating adoption of integrated fixed-detector networks and area monitors. This vertical’s safety demands and zero-tolerance for contamination drive preference for high-accuracy HF sensors and redundant alarm systems.

Regulatory and occupational safety requirements are another powerful catalyst. Hydrogen fluoride carries very low exposure limits and can cause severe health effects in minutes; authoritative bodies set tight exposure thresholds that employers must respect. Those limits drive investments in continuous monitoring and personal protection programs to meet workplace safety rules and to avoid costly shutdowns or enforcement actions.

Technology innovation is also shaping the market. Sensor manufacturers are improving electrochemical cell lifetimes, reducing cross-sensitivity, and delivering plug-and-play smart sensor cartridges that simplify calibration and maintenance. Internet of Things architectures and cloud analytics now allow facility managers to visualize HF trends, correlate alarms with process events, and trigger automated mitigation. Ease of integration with building management systems and process control layers increases the total addressable market.

?????? ???? ????????:

https://www.polarismarketresearch.com/industry-analysis/hydrogen-fluoride-gas-detection-market

Market Challenges

Despite the clear drivers, the HF detection market faces several obstacles. First, HF is highly corrosive and places demanding requirements on sensor materials and housings; maintaining accurate performance in humid or chemically aggressive environments challenges both product design and total cost of ownership. Sensors that detect sub-ppm levels while resisting poisoning by contaminants remain engineering-intensive and relatively costly.

Second, fragmentation of monitoring strategies — from small portable monitors to enterprise fixed systems — creates complexity in procurement and standards. Not all facilities have the technical staff to specify or maintain advanced detection systems, increasing reliance on vendors for lifecycle service and calibration.

Third, supply-chain and calibration logistics can be burdensome. HF sensors and replacement modules are specialized components; ensuring on-site spares, traceable calibration gases, and timely service contracts is operationally intensive, particularly in remote or emerging market locations. Finally, false alarms and cross-sensitivities can erode operator confidence unless devices are correctly selected, installed, and commissioned.

Regional Analysis

North America continues to be a lead market for HF detection due to strict occupational safety enforcement, a large semiconductor and chemical processing base, and high adoption of integrated safety platforms. Corporations here often lead with comprehensive personal protection systems combined with area monitoring. Europe also shows robust demand driven by regulatory stringency and chemical industry activity, with an emphasis on interoperability and compliance documentation.

Asia Pacific represents the fastest-growing opportunity as regional semiconductor expansions, petrochemical projects, and manufacturing modernization take place. Rapid fab construction in parts of East and Southeast Asia is a proximal demand driver for HF detection hardware and services. Growth in India and Southeast Asia is supported by increasing awareness of industrial hygiene but can be constrained by budget sensitivity and uneven service ecosystems.

Latin America, the Middle East, and Africa are at earlier stages of adoption; large-scale projects and energy sector investments create pockets of demand, but broader uptake requires improvements in technical capability and distributor networks. Across all regions, trendlines favor vendors who can offer turnkey systems, local calibration and service, and documentation to support compliance.

Key Companies

The HF gas detection market includes specialized gas-sensor makers, industrial safety OEMs, and system integrators. Notable participants include industry-recognized names that offer HF sensors, fixed and portable detectors, and integration services:

Honeywell (detection sensors and MidAS/Midas smart sensor platforms).

MSA Safety (personal and area monitoring solutions).

Sensidyne (fixed sensor modules and transmitters).

Industrial Scientific (portable gas detection and cloud monitoring).

Dräger (multigas detectors and sensor technologies).

Teledyne/Advanced Specialty Sensors (specialty electrochemical cells).

RKI Instruments (portable and fixed HF monitors).

Yokogawa / other process safety integrators (system integration & alarm management).

Siemens (industrial safety and monitoring subsystems).

NEO Monitors and regional specialists for calibration and service.

These companies compete on sensor accuracy, corrosion resistance, lifecycle cost, and integration with safety information systems. Many offer sensor “cartridge” strategies and service agreements to lower end-user maintenance burdens.

Applications and End-User Priorities

Beyond semiconductor fabs, HF detection is critical in chemical manufacturing, metal finishing, aluminum production, research laboratories, and any facility using fluorinated chemistries. End users prioritize low detection limits, quick response time, ease of calibration, and documented traceability for audits. Personal protection programs increasingly pair wearable single-gas HF monitors with area fixed detectors and ventilation interlocks to deliver layered defense.

Outlook and Opportunities

Market momentum favors bundled offerings: sensor hardware plus lifecycle services plus analytics. As facilities digitize, vendors that provide secure cloud dashboards, predictive maintenance alerts for sensor end-of-life, and automated compliance reporting will gain share. There’s also rising interest in sensor materials and architectures better able to operate in humid or particle-laden atmospheres, creating R&D niches for next-generation HF sensing.

Conclusion

The hydrogen fluoride gas detection market sits at the intersection of stringent safety requirements, concentrated industrial use, and advancing sensor technology. Rising semiconductor capacity, regulatory enforcement, and a general shift toward continuous environmental monitoring underpin durable demand. Overcoming material and service challenges — by delivering corrosion-resistant sensors, streamlined calibration services, and integrated analytics — will define market winners. Providers that can reduce total cost of ownership while ensuring reliable, low-ppm HF detection and compliance documentation will be best positioned to capture a growing share of global deployments as industry teams prioritize worker safety and process resilience.

More Trending Latest Reports By Polaris Market Research: